Stephens Says Union Pacific Investors Have 'Buying Opportunity'

Shares of Union Pacific Corporation (NYSE: UNP) are up more than 2.6 percent on Tuesday trading, after research firm Stephens upgraded its stock from Equal-Weight to Overweight, maintaining a price target of $105.00.

According to a report issued Tuesday, analysts Justin Long and Brian Colley think the year-to-date pullback in the stock’s price (which can also be understood as a contraction in multiples) has created an “attractive” risk/reward profile as fundamentals start to stabilize.

Union Pacific’s stock has lost almost 27 percent since the beginning of the year, and the experts believe “sentiment has also turned increasingly negative (vs. UNP being the darling of the rail sector for years).” With their outlook for fundamentals to start stabilizing, the analysts think “this has created a buying opportunity for a best-in-class operator with a margin/return profile that leads the domestic rails.”

A Look At Valuations

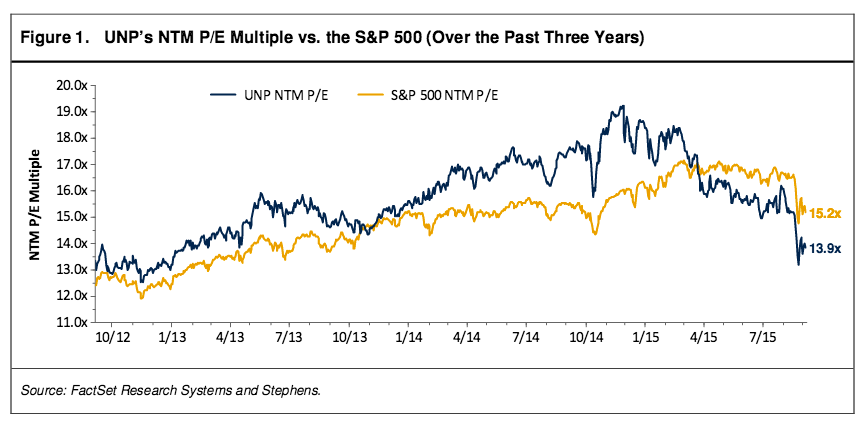

Over the past three years, the company’s NTM P/E multiple has oscillated between 12.6x and 19.2x. Nowadays, it stands around 13.9x “using Street estimates (i.e., towards the lower end of the range),” the note explicated.

On a relative basis (see Figure 1), the NTM P/E multiple has “consistently been above the market (S&P 500) with an average of a 90 bps premium. This changed in March 2015 as valuation slipped below a market multiple with the current discount being 130 bps.”

Source: Stephens

Other Elements In Play

Long and Colley highlighted a few other elements playing out in favor of their investment thesis.

- 1) Fundamentals seem to be stabilizing in the rail industry, following a second-quarter earnings season that was probably "as bad as it gets."

- 2) The experts believe “the primary areas of recent weakness (coal and shale-related products) are very well known.” So, while the prospects for these areas are not particularly promising, they think “a cautious outlook in this area is game-changer to the broader thesis on the stock.”

- 3) Long-term growth drivers remain unchanged – and a recovering housing market should help drive results even higher.

- 4) While competition with BNSF should carry on, the firm believes the relationship is not an “unhealthy” one.

- 5) A 2.6 percent dividend yield and big buyback plans provide nice returns to shareholders.

Image Credit: Public Domain

Latest Ratings for UNP

| Date | Firm | Action | From | To |

|---|---|---|---|---|

| Jan 2022 | Deutsche Bank | Maintains | Buy | |

| Jan 2022 | Susquehanna | Maintains | Positive | |

| Jan 2022 | Raymond James | Maintains | Strong Buy |

© 2025 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Posted-In: BNSF Brian ColleyAnalyst Color Long Ideas Upgrades Price Target Analyst Ratings Trading Ideas Best of Benzinga