A Look Ahead: Westinghouse Air Brake's Earnings Forecast

Westinghouse Air Brake (NYSE:WAB) is preparing to release its quarterly earnings on Thursday, 2025-07-24. Here's a brief overview of what investors should keep in mind before the announcement.

Analysts expect Westinghouse Air Brake to report an earnings per share (EPS) of $2.18.

Westinghouse Air Brake bulls will hope to hear the company announce they've not only beaten that estimate, but also to provide positive guidance, or forecasted growth, for the next quarter.

New investors should note that it is sometimes not an earnings beat or miss that most affects the price of a stock, but the guidance (or forecast).

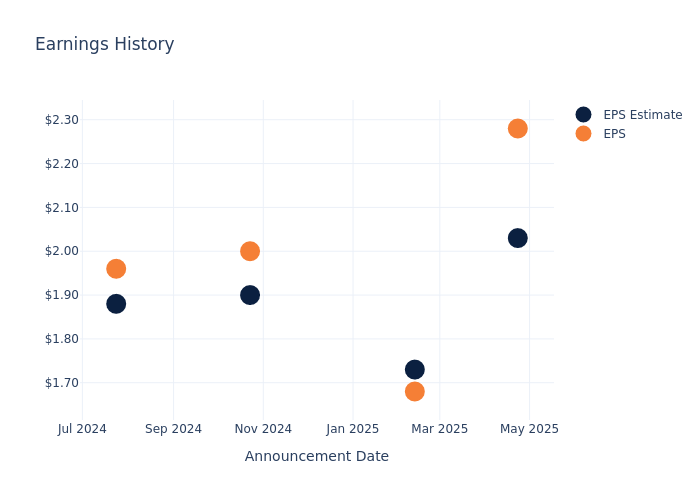

Earnings Track Record

In the previous earnings release, the company beat EPS by $0.25, leading to a 1.87% increase in the share price the following trading session.

Here's a look at Westinghouse Air Brake's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 2.03 | 1.73 | 1.9 | 1.88 |

| EPS Actual | 2.28 | 1.68 | 2 | 1.96 |

| Price Change % | 2.0% | 4.0% | 1.0% | 1.0% |

Tracking Westinghouse Air Brake's Stock Performance

Shares of Westinghouse Air Brake were trading at $211.89 as of July 22. Over the last 52-week period, shares are up 33.53%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analyst Views on Westinghouse Air Brake

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Westinghouse Air Brake.

The consensus rating for Westinghouse Air Brake is Buy, derived from 6 analyst ratings. An average one-year price target of $218.67 implies a potential 3.2% upside.

Peer Ratings Overview

In this comparison, we explore the analyst ratings and average 1-year price targets of Cummins, PACCAR and Oshkosh, three prominent industry players, offering insights into their relative performance expectations and market positioning.

- Analysts currently favor an Buy trajectory for Cummins, with an average 1-year price target of $371.5, suggesting a potential 75.33% upside.

- Analysts currently favor an Neutral trajectory for PACCAR, with an average 1-year price target of $99.5, suggesting a potential 53.04% downside.

- Analysts currently favor an Buy trajectory for Oshkosh, with an average 1-year price target of $124.33, suggesting a potential 41.32% downside.

Overview of Peer Analysis

The peer analysis summary offers a detailed examination of key metrics for Cummins, PACCAR and Oshkosh, providing valuable insights into their respective standings within the industry and their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Westinghouse Air Brake | Buy | 4.53% | $900M | 3.15% |

| Cummins | Buy | -2.73% | $2.15B | 7.78% |

| PACCAR | Neutral | -14.90% | $1.32B | 2.84% |

| Oshkosh | Buy | -9.08% | $399.90M | 2.68% |

Key Takeaway:

Westinghouse Air Brake ranks highest in gross profit and return on equity among its peers. It is in the middle for consensus rating and revenue growth.

Unveiling the Story Behind Westinghouse Air Brake

Westinghouse Air Brake Technologies Corp provides value-added, technology-based products and services for the freight rail and passenger transit industries and the mining, marine, and industrial markets. It provides its products and services through two main business segments: Freight and Transit. The company generates maximum revenue from the Freight segment, which manufactures new and modernized locomotives, provides aftermarket parts and services to existing locomotives, provides components to new and existing freight cars; builds new commuter locomotives; supplies rail control and infrastructure products, including electronics, positive train control equipment, signal design, and engineering services. Geographically, it generates a majority of its revenue from the United States.

Westinghouse Air Brake: Financial Performance Dissected

Market Capitalization Analysis: With a profound presence, the company's market capitalization is above industry averages. This reflects substantial size and strong market recognition.

Positive Revenue Trend: Examining Westinghouse Air Brake's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 4.53% as of 31 March, 2025, showcasing a substantial increase in top-line earnings. As compared to competitors, the company surpassed expectations with a growth rate higher than the average among peers in the Industrials sector.

Net Margin: Westinghouse Air Brake's net margin excels beyond industry benchmarks, reaching 12.34%. This signifies efficient cost management and strong financial health.

Return on Equity (ROE): Westinghouse Air Brake's ROE is below industry standards, pointing towards difficulties in efficiently utilizing equity capital. With an ROE of 3.15%, the company may encounter challenges in delivering satisfactory returns for shareholders.

Return on Assets (ROA): The company's ROA is below industry benchmarks, signaling potential difficulties in efficiently utilizing assets. With an ROA of 1.7%, the company may need to address challenges in generating satisfactory returns from its assets.

Debt Management: Westinghouse Air Brake's debt-to-equity ratio is below the industry average. With a ratio of 0.39, the company relies less on debt financing, maintaining a healthier balance between debt and equity, which can be viewed positively by investors.

To track all earnings releases for Westinghouse Air Brake visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.