A Look at Incyte's Upcoming Earnings Report

Incyte (NASDAQ:INCY) is set to give its latest quarterly earnings report on Tuesday, 2025-07-29. Here's what investors need to know before the announcement.

Analysts estimate that Incyte will report an earnings per share (EPS) of $1.34.

Anticipation surrounds Incyte's announcement, with investors hoping to hear about both surpassing estimates and receiving positive guidance for the next quarter.

New investors should understand that while earnings performance is important, market reactions are often driven by guidance.

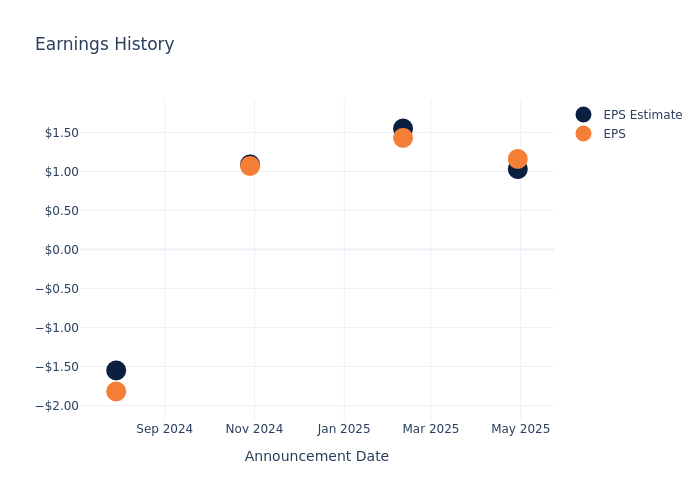

Earnings Track Record

The company's EPS beat by $0.13 in the last quarter, leading to a 3.69% increase in the share price on the following day.

Here's a look at Incyte's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 1.03 | 1.55 | 1.09 | -1.55 |

| EPS Actual | 1.16 | 1.43 | 1.07 | -1.82 |

| Price Change % | 4.0% | -3.0% | 0.0% | -4.0% |

Market Performance of Incyte's Stock

Shares of Incyte were trading at $70.2 as of July 25. Over the last 52-week period, shares are up 3.35%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analysts' Take on Incyte

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding Incyte.

A total of 6 analyst ratings have been received for Incyte, with the consensus rating being Neutral. The average one-year price target stands at $72.33, suggesting a potential 3.03% upside.

Comparing Ratings Among Industry Peers

In this analysis, we delve into the analyst ratings and average 1-year price targets of United Therapeutics, Moderna and Neurocrine Biosciences, three key industry players, offering insights into their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for United Therapeutics, with an average 1-year price target of $356.33, suggesting a potential 407.59% upside.

- Analysts currently favor an Neutral trajectory for Moderna, with an average 1-year price target of $36.83, suggesting a potential 47.54% downside.

- Analysts currently favor an Buy trajectory for Neurocrine Biosciences, with an average 1-year price target of $153.67, suggesting a potential 118.9% upside.

Snapshot: Peer Analysis

In the peer analysis summary, key metrics for United Therapeutics, Moderna and Neurocrine Biosciences are highlighted, providing an understanding of their respective standings within the industry and offering insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Incyte | Neutral | 19.53% | $979.70M | 4.45% |

| United Therapeutics | Neutral | 17.22% | $701.90M | 4.86% |

| Moderna | Neutral | -35.93% | $17M | -9.26% |

| Neurocrine Biosciences | Buy | 11.12% | $563.40M | 0.31% |

Key Takeaway:

In terms of consensus rating, Incyte is in the middle compared to its peers. Incyte has the highest revenue growth among its peers. Incyte also has the highest gross profit. However, Incyte has the lowest return on equity among its peers.

Delving into Incyte's Background

Incyte focuses on the discovery and development of small-molecule drugs. The firm's leading drug, Jakafi, treats two types of rare blood cancer and graft versus host disease and is partnered with Novartis. Incyte's other marketed drugs include rheumatoid arthritis treatment Olumiant (licensed to Lilly), and oncology drugs Iclusig (chronic myeloid leukemia), Pemazyre (cholangiocarcinoma), Tabrecta (lung cancer), and Monjuvi (diffuse large B-cell lymphoma). The firm's first dermatology product, Opzelura, was approved in 2021 for atopic dermatitis and 2022 for vitiligo. Incyte's pipeline includes a broad array of oncology and dermatology programs.

Incyte's Financial Performance

Market Capitalization: With restricted market capitalization, the company is positioned below industry averages. This reflects a smaller scale relative to peers.

Revenue Growth: Over the 3 months period, Incyte showcased positive performance, achieving a revenue growth rate of 19.53% as of 31 March, 2025. This reflects a substantial increase in the company's top-line earnings. As compared to its peers, the company achieved a growth rate higher than the average among peers in Health Care sector.

Net Margin: Incyte's net margin is impressive, surpassing industry averages. With a net margin of 15.03%, the company demonstrates strong profitability and effective cost management.

Return on Equity (ROE): Incyte's ROE excels beyond industry benchmarks, reaching 4.45%. This signifies robust financial management and efficient use of shareholder equity capital.

Return on Assets (ROA): The company's ROA is a standout performer, exceeding industry averages. With an impressive ROA of 2.83%, the company showcases effective utilization of assets.

Debt Management: Incyte's debt-to-equity ratio is below industry norms, indicating a sound financial structure with a ratio of 0.01.

To track all earnings releases for Incyte visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.