Earnings Preview For Timken

Timken (NYSE:TKR) is gearing up to announce its quarterly earnings on Wednesday, 2025-07-30. Here's a quick overview of what investors should know before the release.

Analysts are estimating that Timken will report an earnings per share (EPS) of $1.35.

Timken bulls will hope to hear the company announce they've not only beaten that estimate, but also to provide positive guidance, or forecasted growth, for the next quarter.

New investors should note that it is sometimes not an earnings beat or miss that most affects the price of a stock, but the guidance (or forecast).

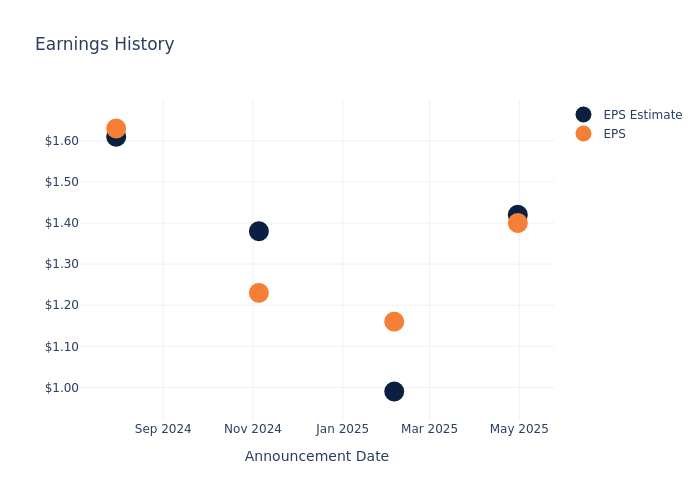

Overview of Past Earnings

In the previous earnings release, the company missed EPS by $0.02, leading to a 0.16% increase in the share price the following trading session.

Here's a look at Timken's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 1.42 | 0.99 | 1.38 | 1.61 |

| EPS Actual | 1.40 | 1.16 | 1.23 | 1.63 |

| Price Change % | 0.0% | -0.0% | 9.0% | -3.0% |

Performance of Timken Shares

Shares of Timken were trading at $81.69 as of July 28. Over the last 52-week period, shares are down 7.21%. Given that these returns are generally negative, long-term shareholders are likely a little upset going into this earnings release.

Analysts' Perspectives on Timken

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding Timken.

A total of 6 analyst ratings have been received for Timken, with the consensus rating being Buy. The average one-year price target stands at $79.83, suggesting a potential 2.28% downside.

Understanding Analyst Ratings Among Peers

This comparison focuses on the analyst ratings and average 1-year price targets of Symbotic, ESCO Technologies and Gates Industrial Corp, three major players in the industry, shedding light on their relative performance expectations and market positioning.

- Analysts currently favor an Outperform trajectory for Symbotic, with an average 1-year price target of $53.33, suggesting a potential 34.72% downside.

- Analysts currently favor an Buy trajectory for ESCO Technologies, with an average 1-year price target of $200.0, suggesting a potential 144.83% upside.

- Analysts currently favor an Outperform trajectory for Gates Industrial Corp, with an average 1-year price target of $24.38, suggesting a potential 70.16% downside.

Summary of Peers Analysis

The peer analysis summary offers a detailed examination of key metrics for Symbotic, ESCO Technologies and Gates Industrial Corp, providing valuable insights into their respective standings within the industry and their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Timken | Buy | -4.20% | $358.70M | 2.73% |

| Symbotic | Outperform | 39.74% | $107.83M | -1.95% |

| ESCO Technologies | Buy | 6.58% | $109.22M | 2.47% |

| Gates Industrial Corp | Outperform | -1.74% | $344.60M | 2.02% |

Key Takeaway:

Timken ranks at the top for Gross Profit and Return on Equity among its peers. It is in the middle for Revenue Growth.

Delving into Timken's Background

The Timken Co designs and manages a portfolio of engineered bearings and industrial motion products, and provides related services. The Company sells products and services to customers in the following market sectors: industrial distribution, renewable energy, automation, automotive original equipment (OE), agriculture/turf, rail, aerospace, auto/truck aftermarket, construction, etc. The company has two reportable segment: The Engineered Bearings portfolio features bearings with precision tolerances, proprietary internal geometries and quality materials. The Industrial Motion portfolio features products such as drives, breathers, seals, automatic lubrication systems, linear motion products, chain, belts, couplings, etc. Key revenue is generated from Engineered Bearings.

Timken: A Financial Overview

Market Capitalization: Exceeding industry standards, the company's market capitalization places it above industry average in size relative to peers. This emphasizes its significant scale and robust market position.

Revenue Challenges: Timken's revenue growth over 3 months faced difficulties. As of 31 March, 2025, the company experienced a decline of approximately -4.2%. This indicates a decrease in top-line earnings. As compared to competitors, the company encountered difficulties, with a growth rate lower than the average among peers in the Industrials sector.

Net Margin: Timken's net margin is below industry standards, pointing towards difficulties in achieving strong profitability. With a net margin of 6.87%, the company may encounter challenges in effective cost control.

Return on Equity (ROE): Timken's ROE excels beyond industry benchmarks, reaching 2.73%. This signifies robust financial management and efficient use of shareholder equity capital.

Return on Assets (ROA): Timken's ROA lags behind industry averages, suggesting challenges in maximizing returns from its assets. With an ROA of 1.21%, the company may face hurdles in achieving optimal financial performance.

Debt Management: Timken's debt-to-equity ratio is notably higher than the industry average. With a ratio of 0.77, the company relies more heavily on borrowed funds, indicating a higher level of financial risk.

To track all earnings releases for Timken visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.