Examining the Future: Marcus's Earnings Outlook

Marcus (NYSE:MCS) is set to give its latest quarterly earnings report on Friday, 2025-08-01. Here's what investors need to know before the announcement.

Analysts estimate that Marcus will report an earnings per share (EPS) of $0.15.

The announcement from Marcus is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

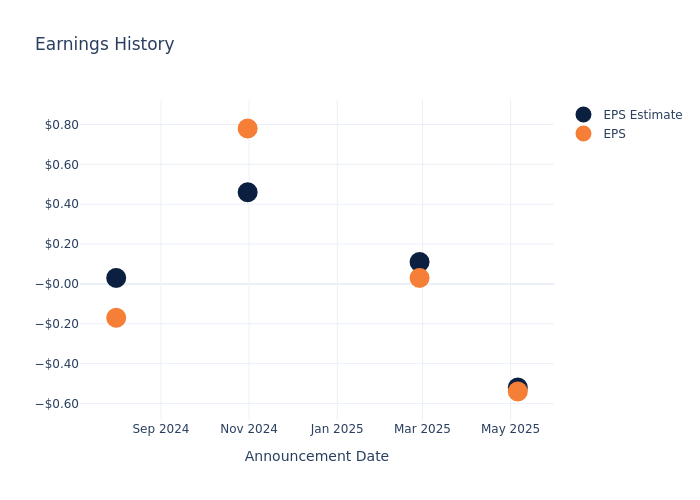

Overview of Past Earnings

During the last quarter, the company reported an EPS missed by $0.02, leading to a 3.83% increase in the share price on the subsequent day.

Here's a look at Marcus's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | -0.52 | 0.11 | 0.46 | 0.03 |

| EPS Actual | -0.54 | 0.03 | 0.78 | -0.17 |

| Price Change % | 4.0% | -1.0% | 9.0% | 4.0% |

Marcus Share Price Analysis

Shares of Marcus were trading at $16.31 as of July 30. Over the last 52-week period, shares are up 23.08%. Given that these returns are generally positive, long-term shareholders are likely bullish going into this earnings release.

Analyst Views on Marcus

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Marcus.

Marcus has received a total of 3 ratings from analysts, with the consensus rating as Outperform. With an average one-year price target of $24.67, the consensus suggests a potential 51.26% upside.

Comparing Ratings with Peers

The following analysis focuses on the analyst ratings and average 1-year price targets of Reservoir Media, CuriosityStream and Sphere Entertainment, three prominent industry players, providing insights into their relative performance expectations and market positioning.

- Analysts currently favor an Buy trajectory for Reservoir Media, with an average 1-year price target of $11.5, suggesting a potential 29.49% downside.

- Analysts currently favor an Buy trajectory for CuriosityStream, with an average 1-year price target of $5.4, suggesting a potential 66.89% downside.

- Analysts currently favor an Buy trajectory for Sphere Entertainment, with an average 1-year price target of $59.75, suggesting a potential 266.34% upside.

Overview of Peer Analysis

The peer analysis summary presents essential metrics for Reservoir Media, CuriosityStream and Sphere Entertainment, unveiling their respective standings within the industry and providing valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Marcus | Outperform | 7.38% | $47.25M | -3.71% |

| Reservoir Media | Buy | 5.80% | $27.17M | 0.74% |

| CuriosityStream | Buy | 25.74% | $8.01M | 0.55% |

| Sphere Entertainment | Buy | -12.68% | $122.25M | -3.77% |

Key Takeaway:

Marcus ranks at the bottom for Revenue Growth among its peers. It also has the lowest Gross Profit margin. However, Marcus has the highest Return on Equity compared to its peers.

All You Need to Know About Marcus

Marcus Corp is engaged in two business segments, which are movie theatres and Hotels and Resorts. The movie theatres segment operates multiscreen motion picture theatres in Wisconsin, Illinois, Iowa, Minnesota, Missouri, Nebraska, North Dakota, Ohio and others, a family entertainment center in Wisconsin and a retail center in Missouri; Hotels and Resorts segment owns and operates full-service hotels and resorts in Wisconsin, Illinois, and Nebraska and manages full-service hotels, resorts and other properties in Wisconsin, Minnesota, Texas, Nevada, California, and North Carolina. It generates maximum revenue from the Theatres segment.

Financial Insights: Marcus

Market Capitalization Analysis: Reflecting a smaller scale, the company's market capitalization is positioned below industry averages. This could be attributed to factors such as growth expectations or operational capacity.

Positive Revenue Trend: Examining Marcus's financials over 3 months reveals a positive narrative. The company achieved a noteworthy revenue growth rate of 7.38% as of 31 March, 2025, showcasing a substantial increase in top-line earnings. As compared to competitors, the company surpassed expectations with a growth rate higher than the average among peers in the Communication Services sector.

Net Margin: Marcus's net margin falls below industry averages, indicating challenges in achieving strong profitability. With a net margin of -11.3%, the company may face hurdles in effective cost management.

Return on Equity (ROE): Marcus's ROE falls below industry averages, indicating challenges in efficiently using equity capital. With an ROE of -3.71%, the company may face hurdles in generating optimal returns for shareholders.

Return on Assets (ROA): Marcus's ROA falls below industry averages, indicating challenges in efficiently utilizing assets. With an ROA of -1.63%, the company may face hurdles in generating optimal returns from its assets.

Debt Management: Marcus's debt-to-equity ratio is below the industry average. With a ratio of 0.88, the company relies less on debt financing, maintaining a healthier balance between debt and equity, which can be viewed positively by investors.

To track all earnings releases for Marcus visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.