Earnings Preview For Hyatt Hotels

Hyatt Hotels (NYSE:H) is set to give its latest quarterly earnings report on Thursday, 2025-08-07. Here's what investors need to know before the announcement.

Analysts estimate that Hyatt Hotels will report an earnings per share (EPS) of $0.66.

The market awaits Hyatt Hotels's announcement, with hopes high for news of surpassing estimates and providing upbeat guidance for the next quarter.

It's important for new investors to understand that guidance can be a significant driver of stock prices.

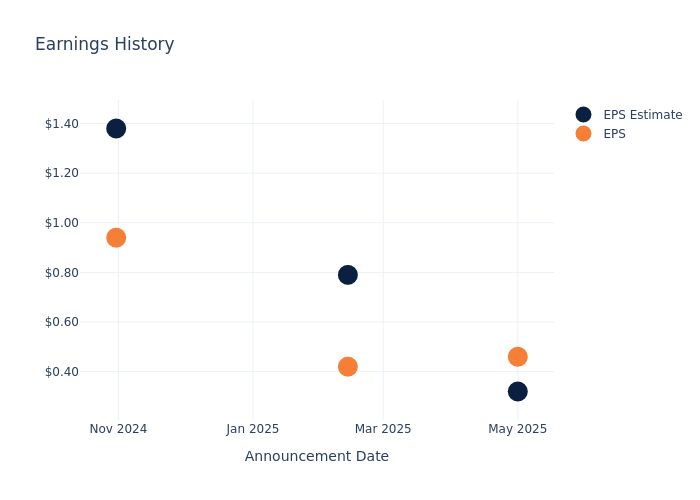

Performance in Previous Earnings

The company's EPS beat by $0.14 in the last quarter, leading to a 3.62% increase in the share price on the following day.

Here's a look at Hyatt Hotels's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 0.32 | 0.79 | 1.38 | 1.17 |

| EPS Actual | 0.46 | 0.42 | 0.94 | 1.53 |

| Price Change % | 4.0% | -3.0% | -0.0% | -1.0% |

Hyatt Hotels Share Price Analysis

Shares of Hyatt Hotels were trading at $136.59 as of August 05. Over the last 52-week period, shares are up 0.96%. Given that these returns are generally positive, long-term shareholders should be satisfied going into this earnings release.

Analysts' Take on Hyatt Hotels

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Hyatt Hotels.

Analysts have given Hyatt Hotels a total of 5 ratings, with the consensus rating being Neutral. The average one-year price target is $149.8, indicating a potential 9.67% upside.

Comparing Ratings with Competitors

The analysis below examines the analyst ratings and average 1-year price targets of Norwegian Cruise Line and MakeMyTrip, three significant industry players, providing valuable insights into their relative performance expectations and market positioning.

- Analysts currently favor an Buy trajectory for Norwegian Cruise Line, with an average 1-year price target of $27.86, suggesting a potential 79.6% downside.

- Analysts currently favor an Buy trajectory for MakeMyTrip, with an average 1-year price target of $118.33, suggesting a potential 13.37% downside.

Snapshot: Peer Analysis

Within the peer analysis summary, vital metrics for Norwegian Cruise Line and MakeMyTrip are presented, shedding light on their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Hyatt Hotels | Neutral | 0.23% | $332M | 0.57% |

| Norwegian Cruise Line | Buy | 6.11% | $1.06B | 2.01% |

| MakeMyTrip | Buy | 5.63% | $193.96M | 4.12% |

Key Takeaway:

Hyatt Hotels ranks at the bottom for Revenue Growth among its peers. It is in the middle for Gross Profit and Return on Equity.

About Hyatt Hotels

Hyatt is an operator of owned (3% of total rooms) and managed and franchised (97%) properties across about 30 upscale luxury brands, which includes vacation brands (Apple Leisure Group, Hyatt Ziva, and Hyatt Zilara), the recently launched full-service lifestyle brand Hyatt Centric, the soft lifestyle brand Unbound, the wellness brand Miraval, and the midscale extended-stay brand Studios. Hyatt acquired Two Roads Hospitality in 2018 and Apple Leisure Group in 2021. The regional exposure as a percentage of total rooms is 63% Americas, 15% rest of world, and 22% Asia-Pacific.

Financial Insights: Hyatt Hotels

Market Capitalization Analysis: Below industry benchmarks, the company's market capitalization reflects a smaller scale relative to peers. This could be attributed to factors such as growth expectations or operational capacity.

Revenue Growth: Hyatt Hotels's revenue growth over a period of 3 months has been noteworthy. As of 31 March, 2025, the company achieved a revenue growth rate of approximately 0.23%. This indicates a substantial increase in the company's top-line earnings. In comparison to its industry peers, the company trails behind with a growth rate lower than the average among peers in the Consumer Discretionary sector.

Net Margin: The company's net margin is below industry benchmarks, signaling potential difficulties in achieving strong profitability. With a net margin of 1.16%, the company may need to address challenges in effective cost control.

Return on Equity (ROE): Hyatt Hotels's ROE lags behind industry averages, suggesting challenges in maximizing returns on equity capital. With an ROE of 0.57%, the company may face hurdles in achieving optimal financial performance.

Return on Assets (ROA): Hyatt Hotels's ROA lags behind industry averages, suggesting challenges in maximizing returns from its assets. With an ROA of 0.15%, the company may face hurdles in achieving optimal financial performance.

Debt Management: The company maintains a balanced debt approach with a debt-to-equity ratio below industry norms, standing at 1.33.

To track all earnings releases for Hyatt Hotels visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.