Insights into Danaher's Upcoming Earnings

Danaher (NYSE:DHR) is set to give its latest quarterly earnings report on Tuesday, 2025-07-22. Here's what investors need to know before the announcement.

Analysts estimate that Danaher will report an earnings per share (EPS) of $1.64.

The market awaits Danaher's announcement, with hopes high for news of surpassing estimates and providing upbeat guidance for the next quarter.

It's important for new investors to understand that guidance can be a significant driver of stock prices.

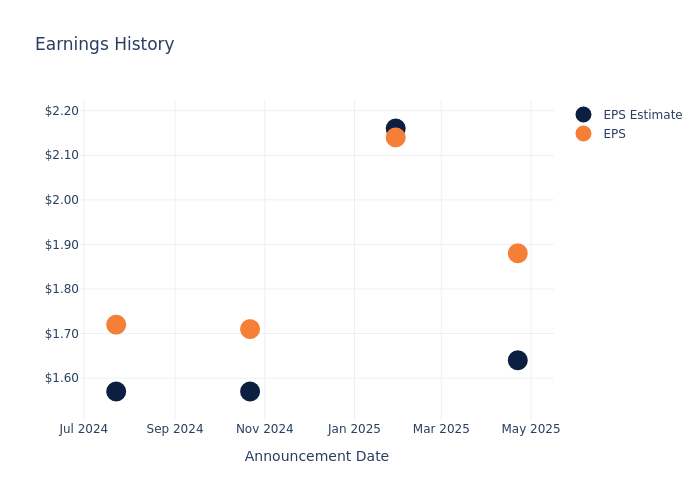

Earnings History Snapshot

During the last quarter, the company reported an EPS beat by $0.24, leading to a 2.21% increase in the share price on the subsequent day.

Here's a look at Danaher's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 1.64 | 2.16 | 1.57 | 1.57 |

| EPS Actual | 1.88 | 2.14 | 1.71 | 1.72 |

| Price Change % | 2.0% | -0.0% | -2.0% | 1.0% |

Market Performance of Danaher's Stock

Shares of Danaher were trading at $190.05 as of July 18. Over the last 52-week period, shares are down 28.65%. Given that these returns are generally negative, long-term shareholders are likely bearish going into this earnings release.

Analysts' Take on Danaher

For investors, staying informed about market sentiments and expectations in the industry is paramount. This analysis provides an exploration of the latest insights on Danaher.

A total of 12 analyst ratings have been received for Danaher, with the consensus rating being Outperform. The average one-year price target stands at $238.5, suggesting a potential 25.49% upside.

Analyzing Ratings Among Peers

The analysis below examines the analyst ratings and average 1-year price targets of Thermo Fisher Scientific, Agilent Technologies and IQVIA Hldgs, three significant industry players, providing valuable insights into their relative performance expectations and market positioning.

- Analysts currently favor an Outperform trajectory for Thermo Fisher Scientific, with an average 1-year price target of $539.08, suggesting a potential 183.65% upside.

- Analysts currently favor an Neutral trajectory for Agilent Technologies, with an average 1-year price target of $136.0, suggesting a potential 28.44% downside.

- Analysts currently favor an Neutral trajectory for IQVIA Hldgs, with an average 1-year price target of $174.0, suggesting a potential 8.45% downside.

Comprehensive Peer Analysis Summary

Within the peer analysis summary, vital metrics for Thermo Fisher Scientific, Agilent Technologies and IQVIA Hldgs are presented, shedding light on their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Danaher | Outperform | -0.95% | $3.51B | 1.90% |

| Thermo Fisher Scientific | Outperform | 0.18% | $4.24B | 3.05% |

| Agilent Technologies | Neutral | 6.04% | $866M | 3.54% |

| IQVIA Hldgs | Neutral | 2.46% | $1.30B | 4.13% |

Key Takeaway:

Danaher ranks at the bottom for Revenue Growth among its peers. It is in the middle for Gross Profit. For Return on Equity, Danaher is at the bottom compared to its peers.

Unveiling the Story Behind Danaher

In 1984, Danaher's founders transformed a real estate organization into an industrial-focused manufacturing company. Then, through a series of mergers, acquisitions, and divestitures, Danaher now focuses primarily on manufacturing scientific instruments and consumables in the life science and diagnostic industries after the late 2023 divestiture of its environmental and applied solutions group, Veralto.

Danaher: A Financial Overview

Market Capitalization: Surpassing industry standards, the company's market capitalization asserts its dominance in terms of size, suggesting a robust market position.

Negative Revenue Trend: Examining Danaher's financials over 3 months reveals challenges. As of 31 March, 2025, the company experienced a decline of approximately -0.95% in revenue growth, reflecting a decrease in top-line earnings. As compared to its peers, the revenue growth lags behind its industry peers. The company achieved a growth rate lower than the average among peers in Health Care sector.

Net Margin: Danaher's net margin is impressive, surpassing industry averages. With a net margin of 16.62%, the company demonstrates strong profitability and effective cost management.

Return on Equity (ROE): The company's ROE is a standout performer, exceeding industry averages. With an impressive ROE of 1.9%, the company showcases effective utilization of equity capital.

Return on Assets (ROA): Danaher's financial strength is reflected in its exceptional ROA, which exceeds industry averages. With a remarkable ROA of 1.22%, the company showcases efficient use of assets and strong financial health.

Debt Management: Danaher's debt-to-equity ratio is below the industry average. With a ratio of 0.32, the company relies less on debt financing, maintaining a healthier balance between debt and equity, which can be viewed positively by investors.

To track all earnings releases for Danaher visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.