Examining the Future: Pilgrims Pride's Earnings Outlook

Pilgrims Pride (NASDAQ:PPC) is set to give its latest quarterly earnings report on Wednesday, 2025-07-30. Here's what investors need to know before the announcement.

Analysts estimate that Pilgrims Pride will report an earnings per share (EPS) of $1.56.

The announcement from Pilgrims Pride is eagerly anticipated, with investors seeking news of surpassing estimates and favorable guidance for the next quarter.

It's worth noting for new investors that guidance can be a key determinant of stock price movements.

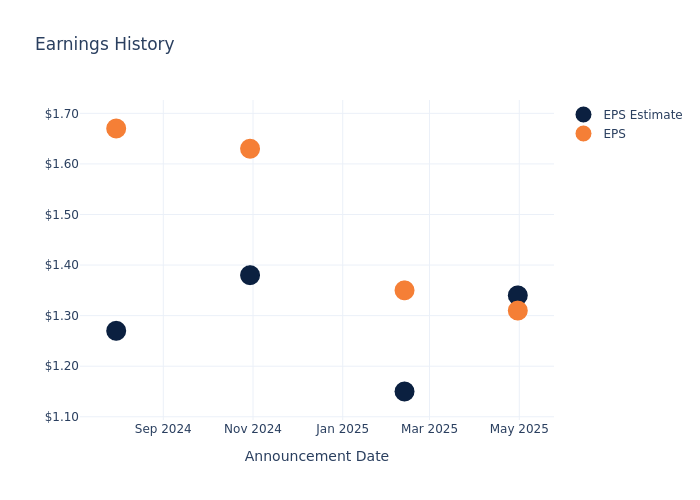

Past Earnings Performance

Last quarter the company missed EPS by $0.03, which was followed by a 14.35% drop in the share price the next day.

Here's a look at Pilgrims Pride's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | 1.34 | 1.15 | 1.38 | 1.27 |

| EPS Actual | 1.31 | 1.35 | 1.63 | 1.67 |

| Price Change % | -14.000000000000002% | 3.0% | 2.0% | 2.0% |

Pilgrims Pride Share Price Analysis

Shares of Pilgrims Pride were trading at $47.65 as of July 28. Over the last 52-week period, shares are up 16.88%. Given that these returns are generally positive, long-term shareholders should be satisfied going into this earnings release.

Insights Shared by Analysts on Pilgrims Pride

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Pilgrims Pride.

A total of 1 analyst ratings have been received for Pilgrims Pride, with the consensus rating being Neutral. The average one-year price target stands at $50.0, suggesting a potential 4.93% upside.

Analyzing Analyst Ratings Among Peers

The following analysis focuses on the analyst ratings and average 1-year price targets of JM Smucker, The Campbell's and Conagra Brands, three prominent industry players, providing insights into their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for JM Smucker, with an average 1-year price target of $116.77, suggesting a potential 145.06% upside.

- Analysts currently favor an Neutral trajectory for The Campbell's, with an average 1-year price target of $35.41, suggesting a potential 25.69% downside.

- Analysts currently favor an Neutral trajectory for Conagra Brands, with an average 1-year price target of $21.93, suggesting a potential 53.98% downside.

Analysis Summary for Peers

The peer analysis summary presents essential metrics for JM Smucker, The Campbell's and Conagra Brands, unveiling their respective standings within the industry and providing valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Pilgrims Pride | Neutral | 2.32% | $554.87M | 8.03% |

| JM Smucker | Neutral | -2.81% | $823.30M | -11.22% |

| The Campbell's | Neutral | 4.47% | $728M | 1.70% |

| Conagra Brands | Neutral | -4.27% | $707.20M | 2.89% |

Key Takeaway:

Pilgrims Pride ranks in the middle among peers for consensus rating. It ranks at the bottom for revenue growth and gross profit, but at the top for return on equity.

Get to Know Pilgrims Pride Better

Pilgrim's Pride is the second-largest poultry producer in the US (59% of 2024 sales), the UK (29% including other European sales), and Mexico (12%). Its UK and European arm also includes pork operations from the 2019 acquisition of Tulip. Pilgrim's sells to chain restaurants, food processors, food distributors, and retail chains. Most of its US and Mexican sales come from fresh chicken, while prepared chicken and pork constitute most of its UK and European sales. JBS owns more than 80% of Pilgrim's Pride's outstanding shares, though it failed to acquire the remaining stake in 2021 after a special board committee deemed that JBS' offer undervalued Pilgrim's Pride.

Key Indicators: Pilgrims Pride's Financial Health

Market Capitalization Analysis: Below industry benchmarks, the company's market capitalization reflects a smaller scale relative to peers. This could be attributed to factors such as growth expectations or operational capacity.

Revenue Growth: Pilgrims Pride's remarkable performance in 3 months is evident. As of 31 March, 2025, the company achieved an impressive revenue growth rate of 2.32%. This signifies a substantial increase in the company's top-line earnings. When compared to others in the Consumer Staples sector, the company excelled with a growth rate higher than the average among peers.

Net Margin: Pilgrims Pride's net margin excels beyond industry benchmarks, reaching 6.63%. This signifies efficient cost management and strong financial health.

Return on Equity (ROE): Pilgrims Pride's financial strength is reflected in its exceptional ROE, which exceeds industry averages. With a remarkable ROE of 8.03%, the company showcases efficient use of equity capital and strong financial health.

Return on Assets (ROA): Pilgrims Pride's ROA surpasses industry standards, highlighting the company's exceptional financial performance. With an impressive 2.74% ROA, the company effectively utilizes its assets for optimal returns.

Debt Management: Pilgrims Pride's debt-to-equity ratio stands notably higher than the industry average, reaching 1.1. This indicates a heavier reliance on borrowed funds, raising concerns about financial leverage.

To track all earnings releases for Pilgrims Pride visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.