Earnings Outlook For Huntsman

Huntsman (NYSE:HUN) will release its quarterly earnings report on Thursday, 2025-07-31. Here's a brief overview for investors ahead of the announcement.

Analysts anticipate Huntsman to report an earnings per share (EPS) of $-0.13.

Investors in Huntsman are eagerly awaiting the company's announcement, hoping for news of surpassing estimates and positive guidance for the next quarter.

It's worth noting for new investors that stock prices can be heavily influenced by future projections rather than just past performance.

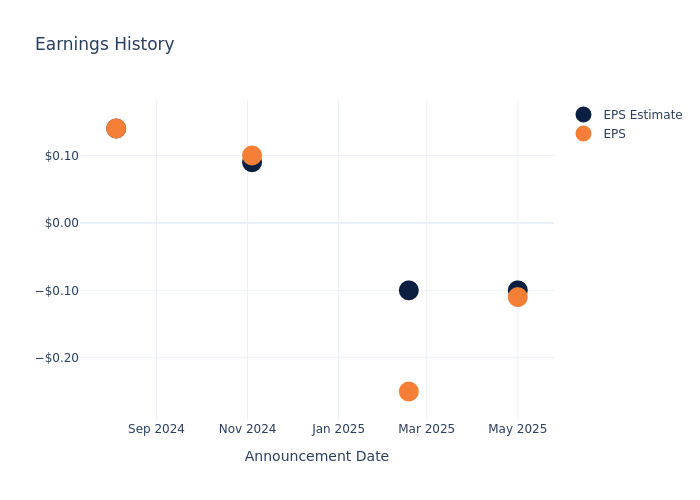

Earnings Track Record

During the last quarter, the company reported an EPS missed by $0.01, leading to a 9.35% drop in the share price on the subsequent day.

Here's a look at Huntsman's past performance and the resulting price change:

| Quarter | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 |

|---|---|---|---|---|

| EPS Estimate | -0.10 | -0.10 | 0.09 | 0.14 |

| EPS Actual | -0.11 | -0.25 | 0.10 | 0.14 |

| Price Change % | -9.0% | 5.0% | -5.0% | -4.0% |

Huntsman Share Price Analysis

Shares of Huntsman were trading at $10.64 as of July 29. Over the last 52-week period, shares are down 57.03%. Given that these returns are generally negative, long-term shareholders are likely bearish going into this earnings release.

Analyst Views on Huntsman

For investors, grasping market sentiments and expectations in the industry is vital. This analysis explores the latest insights regarding Huntsman.

A total of 9 analyst ratings have been received for Huntsman, with the consensus rating being Neutral. The average one-year price target stands at $13.0, suggesting a potential 22.18% upside.

Peer Ratings Overview

This comparison focuses on the analyst ratings and average 1-year price targets of Ingevity, Minerals Technologies and Chemours, three major players in the industry, shedding light on their relative performance expectations and market positioning.

- Analysts currently favor an Neutral trajectory for Ingevity, with an average 1-year price target of $43.0, suggesting a potential 304.14% upside.

- Analysts currently favor an Buy trajectory for Minerals Technologies, with an average 1-year price target of $84.0, suggesting a potential 689.47% upside.

- Analysts currently favor an Neutral trajectory for Chemours, with an average 1-year price target of $14.86, suggesting a potential 39.66% upside.

Snapshot: Peer Analysis

The peer analysis summary presents essential metrics for Ingevity, Minerals Technologies and Chemours, unveiling their respective standings within the industry and providing valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Huntsman | Neutral | -4.08% | $201M | -0.17% |

| Ingevity | Neutral | -16.50% | $113.40M | 9.54% |

| Minerals Technologies | Buy | -2.27% | $136.90M | 2.79% |

| Chemours | Neutral | 0.44% | $236M | -0.68% |

Key Takeaway:

Huntsman ranks at the bottom for Revenue Growth and Gross Profit, with negative percentages compared to peers. It also has the lowest Return on Equity among the group. Overall, Huntsman's performance is weaker compared to its peers in terms of financial metrics.

Unveiling the Story Behind Huntsman

Huntsman Corp is a USA-based manufacturer of differentiated organic chemical products. Its product portfolio comprises Methyl diphenyl diisocyanate (MDI), Amines, Maleic anhydride, and Epoxy-based polymer formulations. The company's products are used in adhesives, aerospace, automotive, and construction products, among others. Its operating segments are Polyurethanes, Performance Products, and Materials. It derives the majority of its revenue from the Polyurethanes segment, which includes MDI, polyols, TPU (thermoplastic polyurethane), and other polyurethane-related products. Its geographical segments are the United States & Canada, Europe, Asia-Pacific, and the Rest of the world.

Huntsman: A Financial Overview

Market Capitalization Analysis: The company's market capitalization surpasses industry averages, showcasing a dominant size relative to peers and suggesting a strong market position.

Revenue Challenges: Huntsman's revenue growth over 3 months faced difficulties. As of 31 March, 2025, the company experienced a decline of approximately -4.08%. This indicates a decrease in top-line earnings. As compared to competitors, the company encountered difficulties, with a growth rate lower than the average among peers in the Materials sector.

Net Margin: Huntsman's net margin excels beyond industry benchmarks, reaching -0.35%. This signifies efficient cost management and strong financial health.

Return on Equity (ROE): Huntsman's financial strength is reflected in its exceptional ROE, which exceeds industry averages. With a remarkable ROE of -0.17%, the company showcases efficient use of equity capital and strong financial health.

Return on Assets (ROA): The company's ROA is a standout performer, exceeding industry averages. With an impressive ROA of -0.07%, the company showcases effective utilization of assets.

Debt Management: With a below-average debt-to-equity ratio of 0.8, Huntsman adopts a prudent financial strategy, indicating a balanced approach to debt management.

To track all earnings releases for Huntsman visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.